The Ultimate Guide to Machine Learning Integration in Fintech: From Strategy to Execution

Introduction

The fintech landscape is undergoing rapid transformation, driven by surging data and increasing demand for faster, smarter, and more personalized financial services. Machine learning integration is a major driver of this shift, offering strategic advantages that go beyond automation to include predictive insights, hyper-personalization, and efficiency. For executives, it's crucial to recognize how these ML capabilities fit into broader business strategies, enhance risk management, and increase ROI. This guide is designed for business leaders, CTOs, and product managers who are seeking a comprehensive roadmap for effective ML adoption, from planning to execution. Key focus areas will include decision points that merit leadership attention, strategic resource allocation, and performance metrics to ensure successful implementation and lead your organization into an AI-powered future.

The Strategic Imperative: Why Fintech Needs Machine Learning

In a sector with tight margins and high customer expectations, fintech machine learning is essential. ML models analyze large datasets in real-time to detect patterns and anomalies that humans would overlook, changing how services are delivered. (Liu, 2025)

Enhancing Fraud Detection with AI-Powered Systems

- Traditional fraud detection relies on rule-based systems that are slow and prone to evasion. AI-powered detection leverages ML to analyze behaviors, devices, and transaction histories to spot anomalies quickly and accurately. This reduces losses, cuts false positives, and improves user experience.

Revolutionizing Credit Scoring with ML

- For decades, credit scoring has been a rigid, backward-looking process. Machine learning algorithms can go beyond traditional credit reports to analyze alternative data sources—like utility payments, rental history, and online behavior—to create a more holistic and dynamic risk profile. This enables financial institutions to serve a broader range of customers, including those who are credit-invisible, fostering greater financial inclusion.

Personalizing Customer Experiences and Services

- In the digital age, a one-size-fits-all approach no longer works. ML in fintech allows for hyper-personalization by analyzing customer data to predict needs and preferences. This can manifest in automated personalized financial advice, tailored product recommendations, or even proactive alerts about spending habits. The result is a more engaging and valuable customer relationship, driving loyalty and lifetime value. [Internal Link: Personalized financial services]

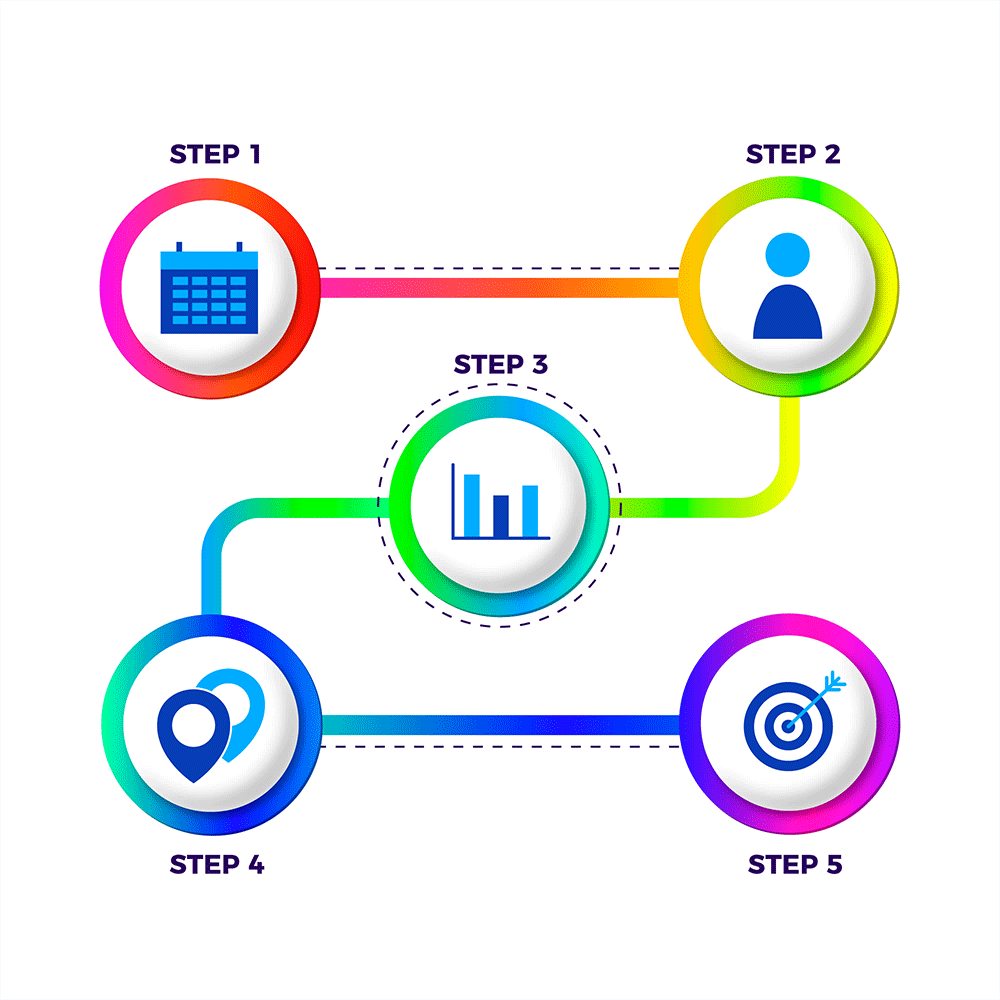

A Phased Approach: The ML Integration Roadmap

Successfully integrating ML is a structured journey, not a single event. It requires a clear strategy, the right technical infrastructure, and a focus on measurable outcomes.

Step 1: Defining Business Objectives and Data Strategy

- Before writing a single line of code, your team must define a clear business problem that ML can solve. Identifying the key metrics you want to improve, such as fraud reduction, customer retention, or loan approval rates, is critical. Once the objective is clear, it is essential to prioritize data strategy by making data your product. Ask yourself: Do you have the necessary data? Is it clean, accessible, and ethically sourced? Treating data as a product involves meticulous data cleaning, labeling, and the establishment of continuous feedback loops, ensuring that your ML models are built on a robust and dynamic foundation. This approach shifts the focus to data-centric AI, revealing that the real competitive edge lies in the quality and handling of your data. A solid data strategy is the cornerstone of successful ML projects in fintech.

- To drive a data-centric culture from the top, executives can take specific actions. Appointing a Chief Data Officer (CDO) can provide leadership and accountability for data strategy across the organization. Establishing a robust data governance framework ensures data quality and accountability, along with promoting consistent data practices. Executives should also champion data literacy initiatives to ensure that all employees understand the value of data in driving business outcomes.

Step 2: Choosing the Right ML Models and Tools

- The choice of model depends on your objective, and understanding the evaluation criteria is paramount. For fraud detection, a supervised learning model like a Random Forest or Gradient Boosting machine might be a good fit, and using metrics such as AUC (Area Under the Curve), precision, and recall will help gauge model effectiveness. When analyzing unstructured customer feedback, a Natural Language Processing (NLP) model is essential, with F1-score and sentiment accuracy as potential evaluation metrics. This is also the stage where you select the right tools and platforms, whether they are open-source libraries like TensorFlow and PyTorch or cloud-based services like AWS SageMaker or Google AI Platform. It's crucial for executives to consider criteria such as scalability, vendor lock-in, compliance, and total cost of ownership when evaluating these ML platforms. These factors are vital in supporting strategic decisions and ensuring the chosen tools align with business objectives.

Step 3: Building, Training, and Validating Models

- This is the core of the technical process. Data scientists use the prepared data to train the chosen models, iteratively tuning parameters to improve performance. Model validation is a critical step to ensure the model's predictions are reliable and generalize well to new, unseen data. Techniques like cross-validation and A/B testing are essential here.

Step 4: Seamlessly Integrating and Deploying Models

- A powerful model is useless if it's not integrated into your existing systems. Deployment requires building a robust, scalable infrastructure that can serve the model's predictions in real-time. This often involves building API endpoints and implementing MLOps pipelines for continuous model monitoring. However, deployment should not be seen as an end point but rather the beginning of an iterative learning system. Setting up monitoring dashboards allows for continuous error analysis and adjustments, while scheduled retraining ensures that the model adapts to new data and maintains its accuracy over time. To ensure long-term success, executive oversight is crucial. Establishing regular review cycles and creating an AI governance board can help executives oversee ongoing model performance and compliance. This governance structure ensures that models remain aligned with organizational goals and adhere to compliance requirements, providing a framework for making data-driven decisions and maintaining ethical standards.

Overcoming Common Challenges in Fintech ML Adoption

While the potential of machine learning in fintech is vast, the path to adoption is not without its hurdles. Proactive planning is key to mitigating these risks.

The Challenge of Data Silos and Data Quality:

- Many financial institutions have their data scattered across legacy systems, making it difficult to create a unified view for a single ML project. Furthermore, incomplete, inconsistent, or "dirty" data can lead to biased or inaccurate models.

Ensuring Compliance and Regulatory Adherence:

- Fintech operates in a highly regulated environment. ML models must be transparent, explainable, and compliant with regulations like GDPR and CCPA. For instance, GDPR's Article 22 highlights the importance of handling automated individual decision-making, demanding explainability to evaluate and understand decisions made by AI systems. Similarly, CCPA addresses consumers' rights to inquire about the personal data used by AI models. PSD2, on the other hand, requires transparency in payment services, reinforcing the need for clear and interpretable AI explanations. The concept of Explainable AI (XAI) is crucial here, as it allows financial institutions to understand how a model arrived at a particular decision, which is often a regulatory requirement. Providing a regulation-to-model table can help translate these legal mandates into technical specifications, ensuring that compliance officers can confidently track and assess model adherence. [External Link: Financial Services Regulators]

- Successfully implementing fintech machine learning requires a multidisciplinary team, including data scientists, ML engineers, domain experts, and business analysts. The demand for these skilled professionals often outstrips supply, making talent acquisition and retention a significant challenge. To address the talent gap, mobilizing a guiding coalition can be instrumental. For instance, consider an early adopter squad within the organization, composed of innovative individuals across different departments, tasked with demystifying ML processes for non-tech stakeholders. By tackling a small, strategic ML project, such as automating customer service responses, the squad can secure a quick win, demonstrating tangible benefits and fostering a sense of urgency and shared ownership in the wider team. This approach not only bridges the gap between technical and non-technical staff but also builds momentum for broader ML adoption.

- Executives should also consider strategic actions to attract and retain ML talent. Establishing partnerships with universities and tech training institutes can provide a steady pipeline of skilled professionals. Additionally, investing in upskilling programs for current employees can enhance internal capabilities and reduce reliance on external hires. Creating incentive structures, such as competitive salaries, opportunities for professional growth, and a focus on work-life balance, can make the organization more attractive to top ML talent and ensure alignment with organizational goals.

Measuring Success: From ROI to Customer Satisfaction

The true value of ML is measured by its impact on the business. Defining key performance indicators (KPIs) and continuously monitoring them is essential.

- Financial Metrics: Look at the direct financial impact, such as reduced fraud losses, lower operational costs, or increased revenue from personalized product sales.

- Operational Metrics: Track improvements in efficiency, such as reduced loan approval times or faster customer service response times.

- Customer-Centric Metrics: Monitor customer satisfaction, churn rates, and engagement levels. A more intuitive and personalized service experience can dramatically improve these metrics.

Conclusion

Machine learning integration in fintech is no longer a futuristic concept; it is the present and future of the financial services industry. From democratizing credit to preventing sophisticated fraud, ML offers a pathway to a more intelligent, efficient, and customer-centric financial ecosystem. The organizations that embrace this transformation by building a solid strategy, investing in the right talent, and focusing on data quality will be the ones that thrive. This guide provides a strategic roadmap, but the journey requires a commitment to continuous innovation and a willingness to embrace data-driven decision-making. The future of finance is here, and it is powered by machine learning.

Next Step: Ready to transform your fintech business with machine learning? [Contact us for a consultation] and let our experts help you build a roadmap for success. [Internal Link: Case Studies]